Corporate Tax Filing: Schedule M-3: Reporting Requirements

This course covers the Schedule M-3 filing and reporting requirements for a consolidated group.

What you will learn

Identify which entities from the financial consolidated group are included/excluded on the consolidated tax return.

Discover the Schedule M-3, Part I reporting requirements for a consolidated group on the consolidated return.

Identify how to report the current/deferred US tax expense for a consolidated group on Lines 1 and 2 of Schedule M-3, part III.

Identify how to report intercompany transactions between members of the consolidated group.

Why take this course?

Corporations with $50 million or more of assets are required to file the more complex Schedule M-3 and completing the Schedule M-3 can be confusing when the corporation prepares consolidated financial statements since some entities eligible for consolidation on a financial basis are not eligible for consolidation on a tax basis. Furthermore, multiple Schedule M-3’s must be filed for the consolidated group, leading to potential “information overload.” It is important to understand the myriad differences between consolidated financial income and consolidated taxable income to navigate through the maze of sometimes conflicting rules.

Other issues to consider include how to compute the total assets and liabilities of a consolidated group reported on Schedule L, form 1120, Balance Sheet per Books, and how to reconcile Retained Earnings per books on Schedule M-2. Since the purpose of Schedule M-3 is to provide detailed information on book-tax differences, it is important to determine the financial information disclosure requirements, including the determination of “book” income versus “taxable Income” for a consolidated group rather than for each member of the consolidated group.

This course covers the Schedule M-3 filing and reporting requirements for a consolidated group, including:

Which entities in the consolidated financial statements are included/excluded on the consolidated tax return.

Schedule M-3, Part I reporting requirements for a consolidated group.

Reconciliation of net income per books to reported on Schedule M-3 to Schedule M-2, Reconciliation of retained earnings on Form 1120.

Schedule M-3, Parts II and III disclosure requirements for the consolidated return, the parent and other members of the consolidated group.

Adjustments for inter-company transactions, temporary versus permanent deferrals on Parts II and III of Schedule M-3.

How to report the current and deferred US tax expense for a consolidated group on Schedule M-3.

Note: Tax compliance for the Schedule M-3 for a corporation that is not part of a consolidated group was covered in the three previous intermediate courses.

A comprehensive example of the Schedule M-3for a consolidated group is provided to reinforce your knowledge of the reporting and tax compliance process of a consolidated group.

Screenshots

Charts

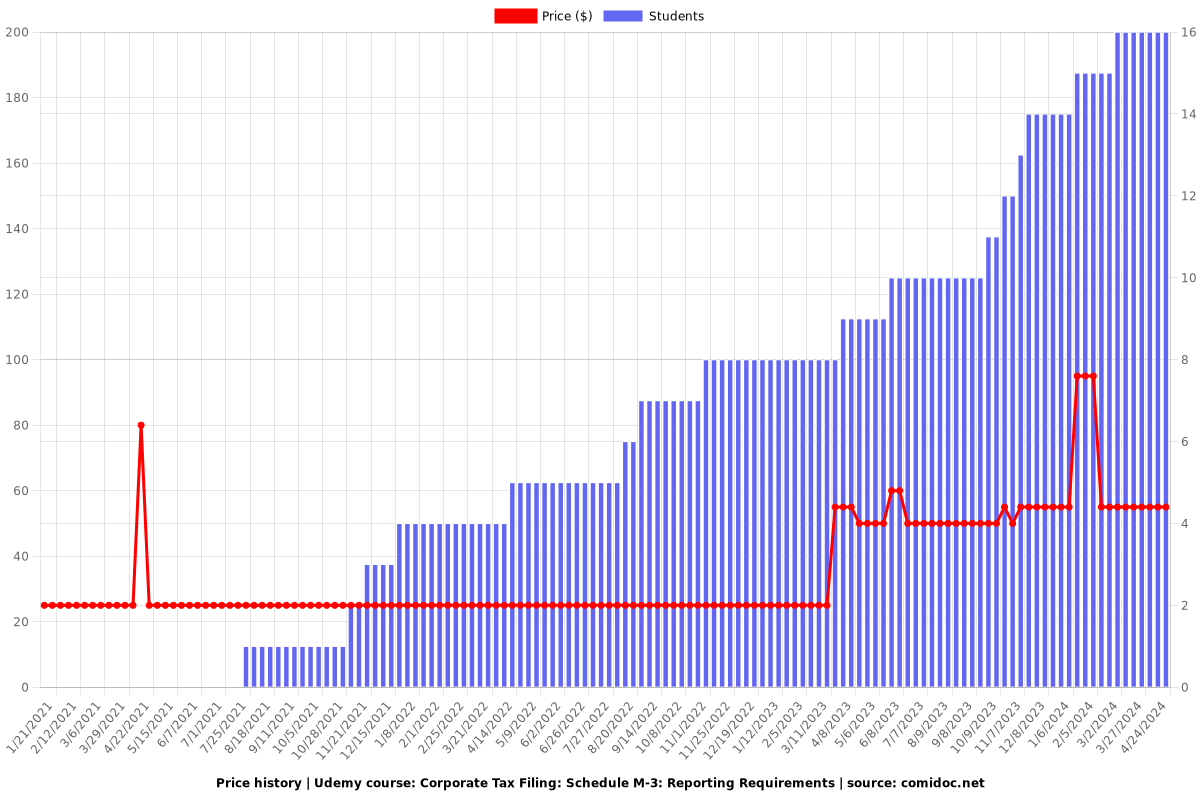

Price

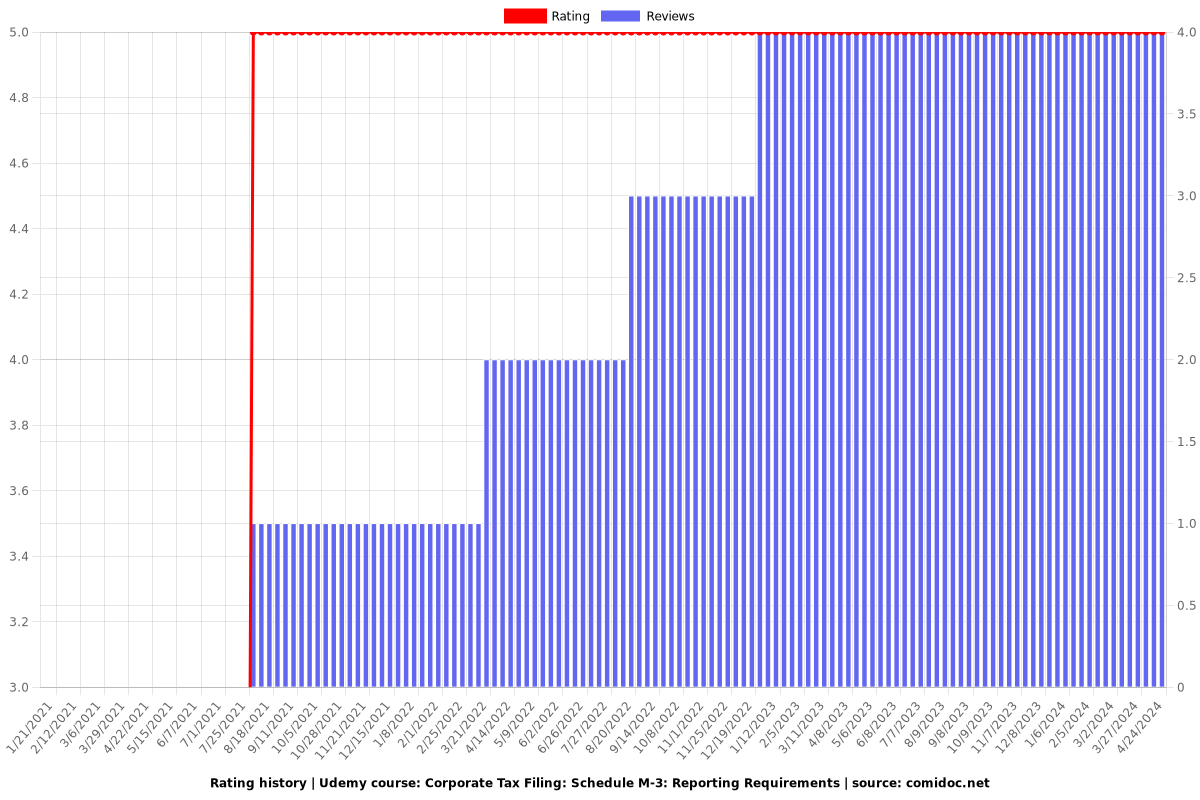

Rating

Enrollment distribution