Time Series for Actuaries

By MJ the Fellow Actuary

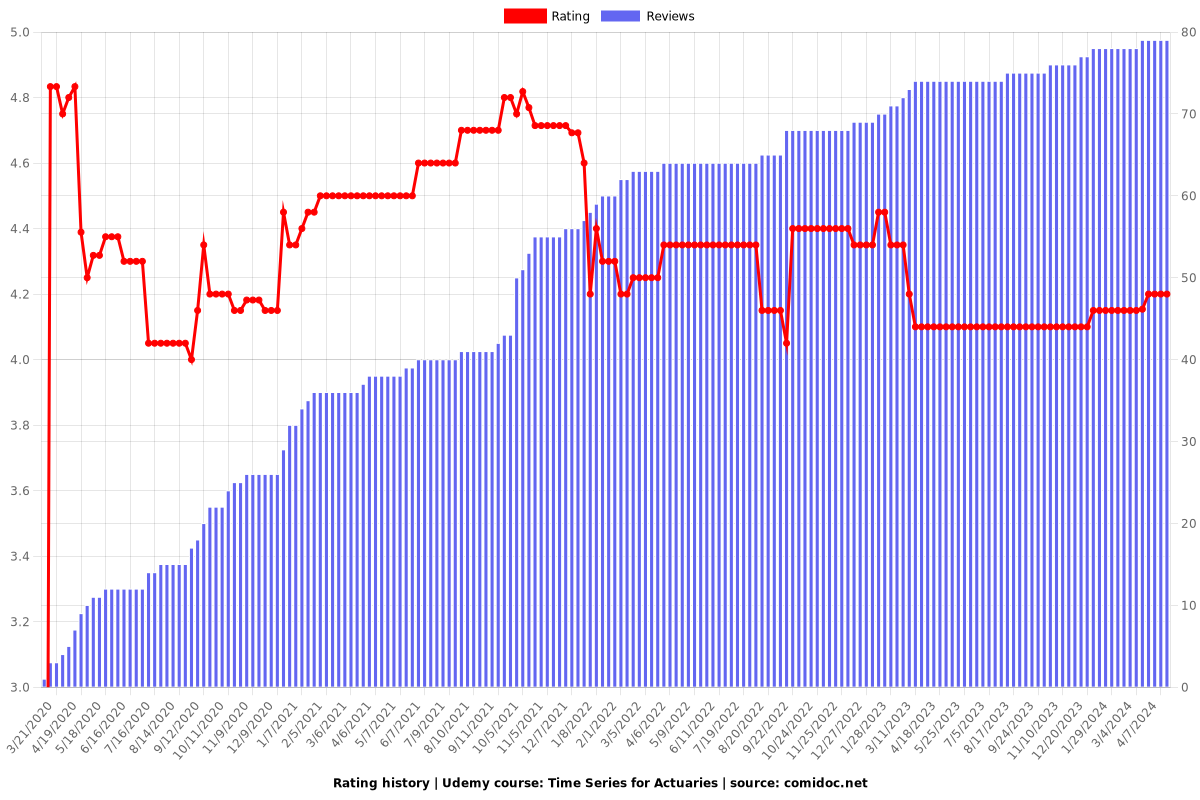

4.20 (79 reviews)

1,956

students

2 hours

content

Mar 2022

last update

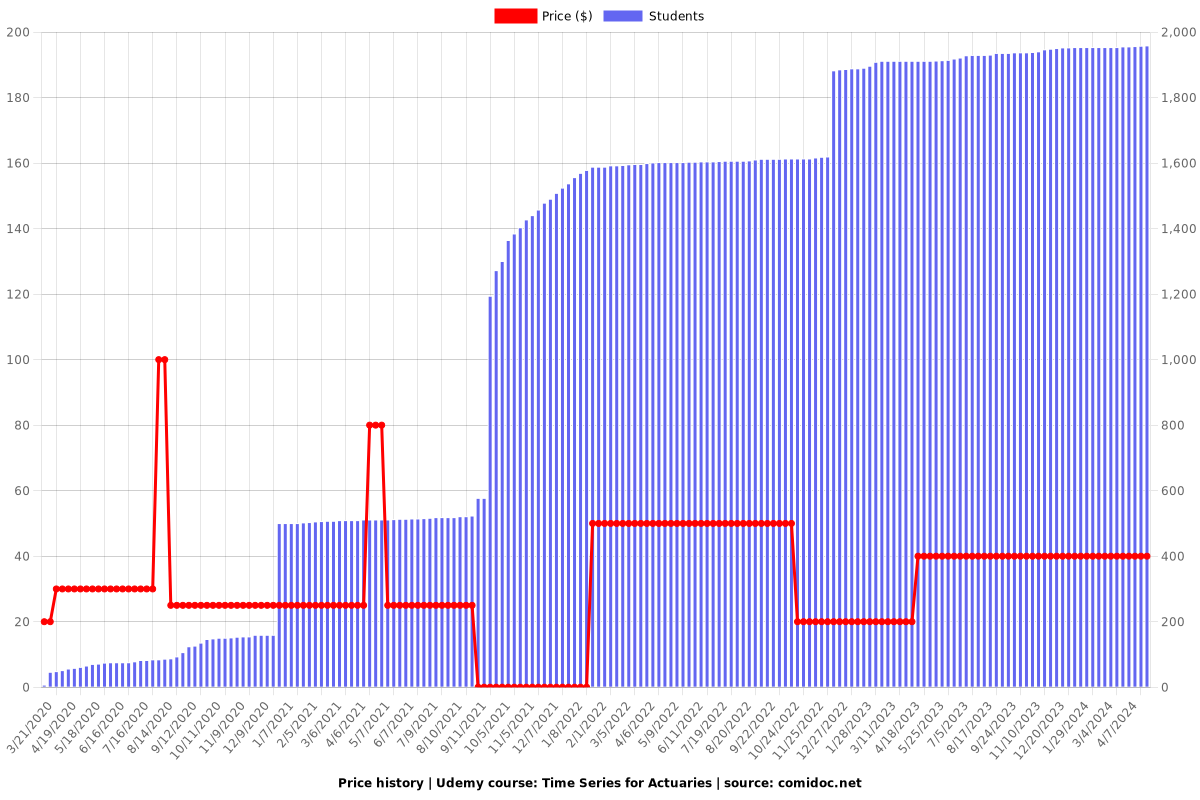

$39.99

regular price

What you will learn

Time Series

Stationary and Markov Property

Autocovariance and Autocorrelation Functions

White Noise

ARIMA Models

GARCH Models

R past paper questions for the Actuarial Exams

Why take this course?

In this course we look at the theory of Time Series that one needs for the Actuarial Exams. We also then do a past paper question from the CS2B exam.

What is a Time Series?

The Stationary and Markov Property

Autocovariance and Autocorrelation functions

Partial Autocorrelation functions

White Noise and other common Time Series

ARIMA

Autoregressive

Integrated

Moving Average

Fitting Time Series to Data

GARCH models for measuring volatility

R Studio Past Exam Question

This course is provided by MJ the Fellow Actuary

Content

Theory

Course Outline

Introduction

Stationary & Markov Property

Autocovariance and Autocorrelation functions

White noise and other common types of time series

ARIMA Time Series

Fitting Time Series to Data

GARCH Models

R Studio

Installing R and Set up

R basics for Actuaries - Part 1

R basics for Actuaries - Part 2

R Past Exam Question

Screenshots

Reviews

Norman

December 11, 2021

I like how MJ uses real-life analogies to explain mathematical concepts; the concepts just come to life naturally! Learning this with a book would have taken twice as long. Thank you!

Rohan

June 9, 2021

The course helped me get a better understanding about time series and its practical implementation.

The course is best for someone who already has some understanding regarding the topics.

Naveet

January 1, 2021

Somehow, I only have access to the first R past exam question and not the other questions. I got the course using the Christmas Code, not sure if that has something to do with access

Pradeep

May 13, 2020

going good so far.MJ has been great at teaching and is very knowledgeable and kind .I can tell the videos I watched over youtube earlier.There should have been more topics compiled under subject CS2.That would have been one stop solution .However is not an issue.Thank you very much Sir for sharing the valuable knowledge!

Neil

March 27, 2020

Really like your courses MJ - thank you for this. Would have liked to see a bit more detail for the written part of this topic - in particular calculation of autocovrainaces and autocorrelations. All in all very helpful, nonetheless.

PS - the installation part was painful :)

Joshua

March 23, 2020

Could we see more examples on the theory side of things regarding how to prove stationarity from examples, invertibility, how to identify different models etc?

Charts

Price

Rating

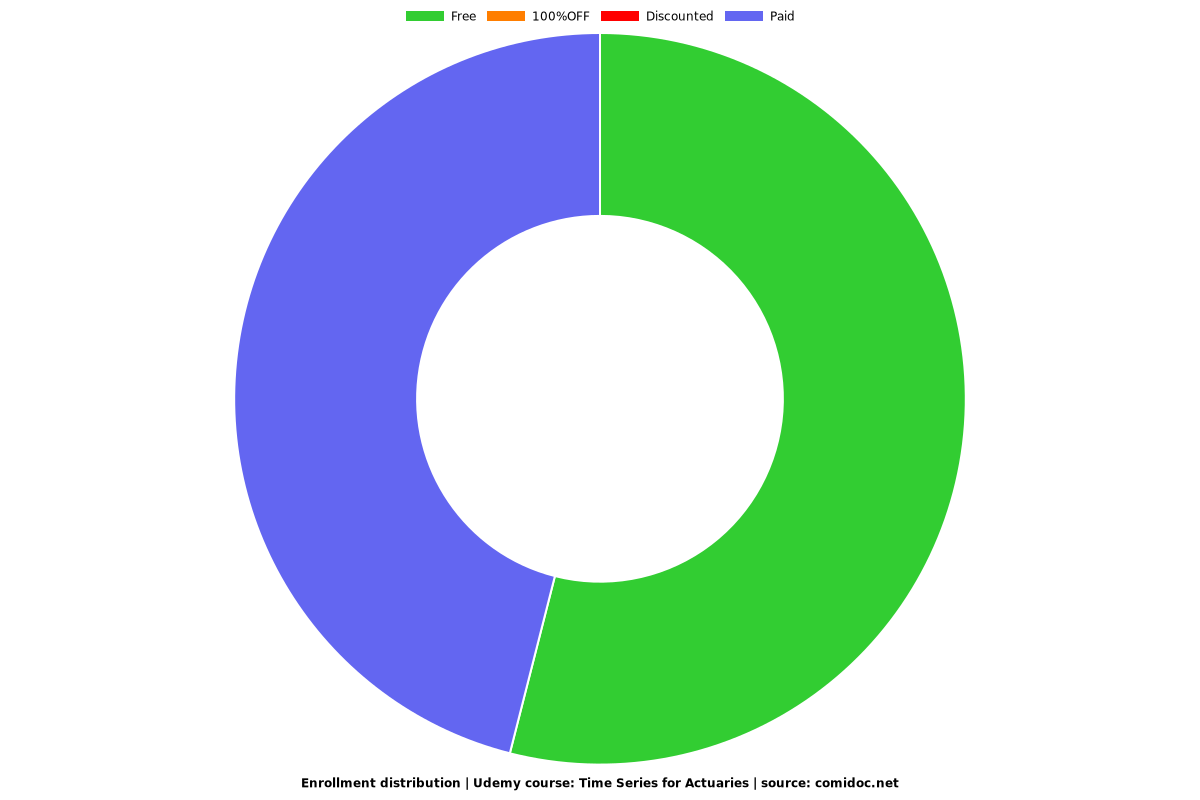

Enrollment distribution

Related Topics

2884172

udemy ID

3/18/2020

course created date

3/21/2020

course indexed date

Bot

course submited by